Date:

30.04.2026

Vedicard – Communication Partner of Baltic Fintech Days 2026

Vedicard is pleased to announce that we are a communication partner of Baltic Fintech Days 2026, taking place on 12–13 May at Hanzas Perons, Riga.

Each year, Vedicard brings together industry professionals from various countries through the Payment Market Conference. However, this year is particularly special — Riga will host one of the region’s largest fintech events, gathering a wide audience of industry experts, startups, investors, technology providers, and fintech enthusiasts.

Baltic Fintech Days 2026 promises to be a large-scale and content-rich event, and Vedicard strongly recommends attending.

Date:

06.11.2025

Vedicard Attended The Payments Association EU & Paynt Event in Riga

On November 6, 2025, Vedicard was honored to attend The Payments Association EU & Paynt event in Riga as invited payment industry specialists. The event brought together leading fintech and payments professionals from across the Baltics and Europe to discuss the future of the industry and explore new collaboration opportunities.

The event was hosted by The Payments Association EU in partnership with Paynt and served as an introduction of the Association to the Latvian and Baltic fintech ecosystem. As one of Europe’s leading payments industry associations, The Payments Association EU is actively expanding its network and seeking strategic partners across the region.

The agenda featured valuable insights from key industry leaders. Tina Luse from Fintech Latvia Association provided a clear overview of the rapid development of Latvia’s fintech ecosystem. Jānis Katkovskis from Latvijas Banka highlighted the practical benefits of Non-bank Direct SEPA Access, while Dina Buse from the Ministry of Finance shared insights into Latvia’s new fintech strategy and its ambitions as a growing European fintech hub. The opportunities and benefits of joining The Payments Association EU were presented by Thibault de Barsy.

The event gathered representatives from major international and regional companies, including Visa, Worldline, PwC, Wallester, Tietoevry, Brite Payments, LexisNexis, DECTA, Magnetiq Bank, Rietumu Banka and many others, creating an excellent platform for meaningful discussions and future partnerships.

For Vedicard, participation in this event reinforced our commitment to contributing to the development of the Baltic payments ecosystem, strengthening international cooperation, and building long-term strategic partnerships within the European fintech community.

Date:

05.06.2025

VediCard at Money20/20 Europe 2025 – A Milestone Year with Our Own Stand

From June 3–5, 2025, VediCard participated in Money20/20 Europe in Amsterdam, one of the world’s most influential fintech and payments industry events. This year marked a special milestone for us — for the first time, VediCard had its own dedicated spot at the Latvia booth, welcoming attendees, partners, and new connections from across the global financial ecosystem.

From the very first day, the energy was incredible. With thousands of fintech, payments, banking, and technology professionals gathering from across Europe and around the world, Money20/20 once again proved to be one of the most significant events in the financial industry calendar.

The days were filled with back-to-back meetings, spontaneous conversations, new ideas, and valuable insights. So many discussions, new contacts, and inspiring exchanges — intense, busy, but truly rewarding days. Having our own space to

represent VediCard and share our expertise in payment solutions, fintech innovation, and EU-compliant financial infrastructure made this year especially meaningful.

We extend our sincere gratitude to Latvijas Investīciju un attīstības aģentūra (LIAA) — especially Jēkabs Groskaufmanis, Elita Krone, and Gustavs Lapins — for organizing an outstanding Latvia booth. The stand was bold, professional, and

beautifully represented Latvia on the international stage.

It was a pleasure reconnecting with our valued partners, including Visa (Evita Kalmane-Pivkina), WALLETTO team, and Wallester team, as well as meeting many new collaborators and industry professionals.

We also appreciated meaningful conversations with Tina Luse (Fintech Latvia Association), Marine Krasovska (Latvijas Banka), and Artjoms Asatrjans and Reinis Znotins (The Latvian Blockchain Association – LBAA).

A special thank you to our fellow Latvian exhibitors — Finchecker, Bonusukarte.lv, Money Express, Forse AI, Crassula, Tailwindapp.eu, and 11xBoosters — for sharing this global platform together.

Money20/20 Europe 2025 once again demonstrated the scale, innovation, and global collaboration shaping the future of finance. We returned home inspired, with fresh ideas, strengthened partnerships, and exciting new opportunities ahead.

See you next year!

Date:

23.05.2025

Vedicard Joined the Largest Latvian Business Delegation to Germany

From May 23 to 25, 2025, Vedicard joined the largest Latvian business delegation to Germany, bringing together more than 180 entrepreneurs and organizations alongside Prime Minister Evika Siliņa and Minister of Economics Viktors Valainis for an official working visit to Hamburg and Rostock.

Vedicard was proud to represent Latvia’s fintech industry and showcase how we support businesses and institutions in building modern, secure, and efficient payment solutions that are fully compliant with EU regulations and prepared for future challenges.

Our expertise lies in information technologies, IT project management, and business development, with a strong focus on finance, payment solutions, cooperation with international payment schemes, and close collaboration within the fintech ecosystem.

During the visit, the delegation explored innovation clusters, participated in high-level discussions, and engaged with German partners to strengthen economic cooperation between Latvia and Germany. The program highlighted Hamburg’s strong financial infrastructure and Rostock’s dynamic innovation and energy ecosystem, offering valuable insights into future collaboration opportunities.

We extend our sincere gratitude to Prime Minister Evika Siliņa and Ministerpräsidentin Manuela Schwesig for their leadership, to Minister Viktors Valainis, Andreas Dressel, and Wolfgang Blank for supporting fintech cooperation initiatives, and to the Investment and Development Agency of Latvia (LIAA) for organizing and leading this impactful delegation.

We return to Latvia with fresh insights, new connections, and strong confidence that this visit marks the beginning of long-term partnerships and innovative cross-border projects.

Date:

03.04.2025

Vedicard Team Attended Baltic Fintech Days 2025 in Vilnius

On April 2–3, 2025, the Vedicard team participated in Baltic Fintech Days 2025, one of the most significant fintech events in the Baltic region, held in Vilnius, Lithuania.

The conference brought together over 1,000 industry professionals, including fintech leaders, investors, regulators, and technology experts from across Europe and beyond.

The two-day program featured keynote speeches and panel discussions covering key topics such as payment innovation, regulatory developments, AI applications in financial services, open finance, digital identity, and the future of the European fintech ecosystem.

Vedicard was represented at the event by Indra Ķešāne, Ludmila Bērziņa, Baiba Mileiko and Ģirts Aizstrauts.

Attending Baltic Fintech Days provided valuable opportunities to gain insights from industry leaders, strengthen international connections, explore emerging technologies, and identify potential partnerships for future collaboration.

We appreciate the opportunity to be part of such a dynamic and forward-looking fintech community and look forward to applying the insights gained to further enhance Vedicard’s innovation and service development.

Date:

10.03.2025

Vedicard at Money 20/20 Europe

We at Vedicard are excited to participate in Latvias booth in Money 20/20 that will take place in 03-05.06 in Amsterdam, if you are nearby - come and say Hi! We are in booth 7C70

More info on event https://europe.money2020.com/

Excited!

Projekts realizēts saskaņā ar Vedicard un LIAA noslēgto līgumu: Latvijas nacionālo stendu informācijas, komunikācijas un tehnoloģijas nozares starptautiskajā izstādē “Money 20/20 Europe” Nīderlandē, kas notiks no 03.06.2025 - 05.06.2025,

Nr. 17.1-1-L-2024/85

Date:

10.03.2025

Payment Market Conference Riga 2025

With the event just a month away, the excitement is only set to grow. As the countdown continues, the anticipation and enthusiasm will undoubtedly reach new heights in our events team that is working towards making this event one to remember.

Same venue, interesting speakers, different topics to explore!

Latest information and updates will be published in event page.

Stay tuned!

Date:

11.02.2025

ATM Pooling is Establishing Itself in Europe

By EPCA Members: rieger.fi & Galitt

Europe’s ATM networks are gradually changing with new ownership and operating models emerging in several countries. Despite the decline in cash usage, smaller, more efficient ATM networks are expected to be with us for many years to come.

Date:

28.11.2024

ECOM 21

We are attending ECOM21 = event to meet many people including

Visa

Mastercard

WALLETTO

Tietoevry

D8 Corporation

DECTA

Latvijas Pasts

Magnetiq Bank

Paynt

and other representatives of financial sector, colleagues and cooperation partners.

Today is a second day of event - see you there! Excited!

Date:

22.11.2024

Season's Final Fintech Breakfast!

Yesterday, I had the pleasure of participating in the season’s final Fintech breakfast, hosted by the #Fintech Latvia Association, at #Ellex Legal. A special thanks to @Tina Luse and the team for organizing this exceptional event, focusing on Fintech Strategy Development: Capital Availability and Support Instruments.

The morning was filled with inspiring discussions, valuable insights, and a shared passion for driving the future of fintech in Latvia.

Special thanks to:

👏 Marine Krasovska and Latvijas Banka (Bank of Latvia)

👏 Ekonomikas ministrija/Ministry of Economics

👏 Ellex Legal

👏 ALTUM

👏 Latvian Private Equity and Venture Capital Association (LVCA)

👏 Mintos

👏 Tenity

Thank you Jānis Līcis from #Paynt for the engaging conversations in payment market and to Jānis Svemps from #Altum for sparking new ideas for development.

Thank you to all from #Vedicard, for the opportunity to be part of this inspiring event. I’m already looking forward to next year’s breakfast sessions! ☕

#FintechLatvia #Networking #Innovation #StrategyDevelopment #Collaboration

Date:

22.10.2024

EPCA meets again for October forum

Vedicard took part in EPCA October forum in Olso. That was organized by EPCA Norway member - Avantio. Shared latest updates from each of corresponding EPCA member country. News and trends in payment market, a lot of information in very compact schedule.

Thank you very much , Morten, for hospitality and well-organized meeting!

Date:

07.10.2024

Payment Market Conference RIGA 2025 - Save the date!

Our past conferences have been packed full of valuable information and outstanding networking opportunities, and we know this conference will continue the tradition.

250+ participants and 20+ speakers from schemes, banks, fintechs, regulatory, processors…

Spend 2 days finding out the latest information on Card scheme news, Regulatory issues, updates, Cloud solutions, Open banking solutions, Digital currency, Crypto issues, user experience and case studies, and much more...

More information coming soon.

Looking forward to see you at the conference!

Does your company want to become a conference sponsor or speaker? Write us – events@vedicard.eu we will gladly provide more info.

Date:

06.06.2024

Money 20/20 Europe

Date:

20.04.2024

EPCA Forum, 18-19 April 2024, Madrid

Date:

22.12.2023

Year of 2023

From all of us - we wish you to have Merry Christmas and a Happy New year!

Date:

28.10.2023

EPCA Forum Riga

The twelve members of the EPCA met for their year 23 Forum in Riga, Latvia hosted by Vedicard – our Latvian member and organised by Mikko Rieger, Chairman. A very enjoyable session was held with presentations from those present.

Emmanuel Caron was elected as Chairman for 2024 and the next Forum will be held in Spain hosted by Nalba.

https://europeanpaymentadvisors.com/news/

Date:

23.08.2023

Payment Market Conference RIGA 2023

Soon, a little more than after 2 month we will meet again in Payment Market conference in Riga!

Same venue, difference speakers, different topics to explore!

Latest information and updates will be published in event page.

Stay tuned!

Date:

19.04.2023

Partner event

Yesterday VediCard as a long term cooperation partner was invited to participate in a presentation of airBaltic 40-th Airbus A220-300, that honors Latvias cultural heritage - XXVII Nationwide Latvian Song and XVII Dance Festival, that will take place this year and will celebrate 150 years of this tradition.

Happy to participate in this event, meet our partners, and looking forward to the week of song and dance celebration in Riga this summer!

Date:

13.04.2023

ECOM'21

We are happy to have face to face events back, we did really miss that. By our faces you can see how happy we and our payment card business colleagues are to finally meet in person and share news and thoughts. Thank you for this event ECOM21!

Date:

13.04.2023

New payment card in Latvia

We at Vedicard have received several requests to share more information on what projects we participate and what are our customers. ❓

Yesterday provided a great opportunity to share with you one of the projects where we as consultants participated from the very beginning.

And here is the result 🎉 - new payment card 💳 has entered the Latvian market, created in cooperation with Latvijas Pasts, Visa and Wallester.

Date:

06.06.2022

Already or Only 10?

Traditions are to be maintained, especially those who repeat once per year. For Veidcard 10 years celebration we did choose a place with corresponding name, Palace of celebration, on banks of Daugava river. We did invite our long term partners and persons closest to us. Together with gratitude for partnerships developed we did celebrate our colleagues too, with whom we are happy to share our working days together. A lot of books can be written on topics discussed in the evening, where we did not limit ourselves to ordinary talks over the coffee in the office, or talk to you in a minute for a minute format.

We did take our time to imagine what else could we need too.

Traditions are making you stronger - in one evening by celebrating Vedicard 10-th year we have obtained extra strengths to proceed and step into our future.

Thanks to all who were with us in years that passed and shared those together!

Together we stand, together we can, we shall succeed!

Full steam ahead!

Date:

27.12.2021

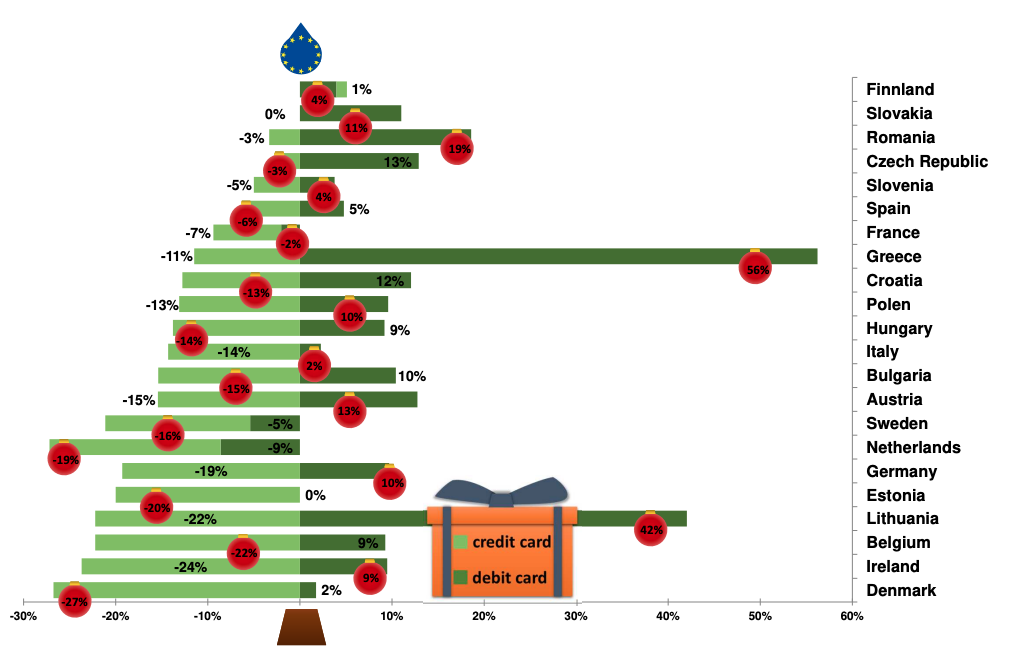

Infographic | Corona and the European card business

Interesting article by Dr. Hugo Godschalk (General Manager and partner of PaySys Consultancy GmbH).

Did the pandemic affect the European card business?

In the first year of the new Corona era, the pandemic has shaken up consumer behaviour and thus payment habits in Europe. The demand for cash has increased, while its use as a means of payment has decreased. The volume of card payments (in euros) of cards issued in the EU-27 has declined slightly (minus 0.8% compared to 2019), despite the substitution of cash at the checkout and growth in e-commerce. However, the development is very heterogeneous within the EU in the member states, such as in Germany with plus 1.1% (incl. ELV) and in neighbouring Holland, by contrast, with minus 9.8%. The varying severity of the lockdowns has left its mark.

In the card business, however, it is noticeable that in almost all member states the credit card business (incl. so-called charge cards or delayed debit cards) has suffered considerably from the consequences of the pandemic: On average minus 13%. Obviously, the credit card continues to be the instrument preferred in the travel & entertainment segment and was particularly affected by the lockdowns. The debit card, on the other hand, was able to hold its own or even expand its position (at the expense of cash) with a growth of 4% in the payment of goods and services for daily needs. Obviously, not all cards are the same in the mind of the consumer.

The opposite development of debit and credit cards in the EU would theoretically lend itself to a nice pyramid-like graph. Our infographic is based on the ECB’s country statistics (data input by the respective central banks – as of July 2021). We have omitted some countries because there is no data for the card business there (Cyprus, Latvia, Malta) or apparently it is still not possible to distinguish between credit and debit cards, e.g. in Portugal. For Germany, we have added the ELV card volume (signature-based direct debits generated by using the domestic girocard) that is missing in the statistics.

Likewise, there is no added value in presenting the figures for Luxembourg, as the card sales volume recorded there is mainly generated by non-resident cardholders. The methodology of the ECB statistics is based on the location of the respective payment service provider. On the issuing side, it can still largely be assumed that the location of the card issuer and the cardholder are identical. Cross-border card issuing is still a relatively rare phenomenon (with the exception of Luxembourg and Lithuania).

We have tried a lot, but somehow our Christmas tree has unsightly bare spots and some extremely long branches. What is going on?

In Lithuania, we have had the same problem since 2020 as described above for Luxembourg. As a result of the Brexit, some issuers from the UK have settled there, including the e-money institution Payrnet, which has taken over the card business of Wirecard Card Solutions. The card volume recorded so far in the UK is immediately significant in a relatively small member state (plus 42%). However, it has nothing to do with the Lithuanian card business, as most of this issuer’s cards are issued cross-border.

The second outlier is Greece with 56% (!) growth in debit card business. To curb tax evasion, the Greek government imposed card acceptance for most face-to-face transactions several years ago. Even the rent for a beach lounger can be paid by card almost everywhere. In addition, discounts in income tax were granted if one could prove cashless payments. At the time, this led to a jump in card sales statistics, but this effect has long since died down. To our knowledge, there are also no new coercive measures to encourage cashless (card) payments. A representative of a large Greek acquirer recently told me that card payments at POS in the face-to-face business have more or less stagnated in 2020. That doesn’t fit with the 56% increase in card payments on the issuing side unless Greeks made mass purchases with cards abroad and/or remote in the Corona year. The solution to the puzzle is probably a major error in the payment transaction statistics of the Bank of Greece. The statistics are inconsistent in several places. For example, in the same statistic, the number of POS transactions of Greek cards domestically and abroad in 2019 is given as 691 million, and elsewhere the number of only domestic POS transactions of these cards is given as 960 million. This does not add up. One or both numbers are wrong. A transposition of numbers? We have asked the central bank in Athens. The answer is still pending. We are pretty sure, this branch in our Christmas tree will soon be trimmed down considerably.

We’ll see what new insights the second Corona year brings us. Until then, we wish you a Merry Christmas, with a hopefully more beautiful Christmas tree.

Date:

07.12.2021

2021

Year to remember indeed!

We would like to wish all our partners and customers to have a Merry Christmas and a Happy new 2022 Year of water tiger!

May strength, braveness of tiger and energy of water described as kindness, curiosity and intuitive intelligence be with us in 2022!

Date:

31.05.2021

Our location update

After almost 10 years in previous location and due to increase of business and employees count we have decided that it is time to seek for new office location. New office is still in the center of Riga with splendid views. That seems to help on daily tasks (or maybe not so much) on sunny days like this. Our new office address is Elizabetes 65-16, Riga, LV-1050.

Date: 31.05.2021

Panel discussion on opportunities and threats linked to Buy now Pay later

The European Payments Consulting Association (EPCA) is joining forces with the European Women Payments Network (European Women Payments Network (EWPN)) on Thursday 10 June to hold a panel discussion on opportunities and threats linked to #buynowpaylater.

To learn more about the event and register follow the link: https://lnkd.in/dGR8imf.

Panelists:

Szilvia Egri – FemTechLab and Country Ambassador of #EWPN Hungary

Marco Fava – CleverAdvice

Mikko Rieger – Consulting in Payments

Chris Jones – PSE Consulting

Moderator:

Ronald te Velde

Date: 01.04.2021

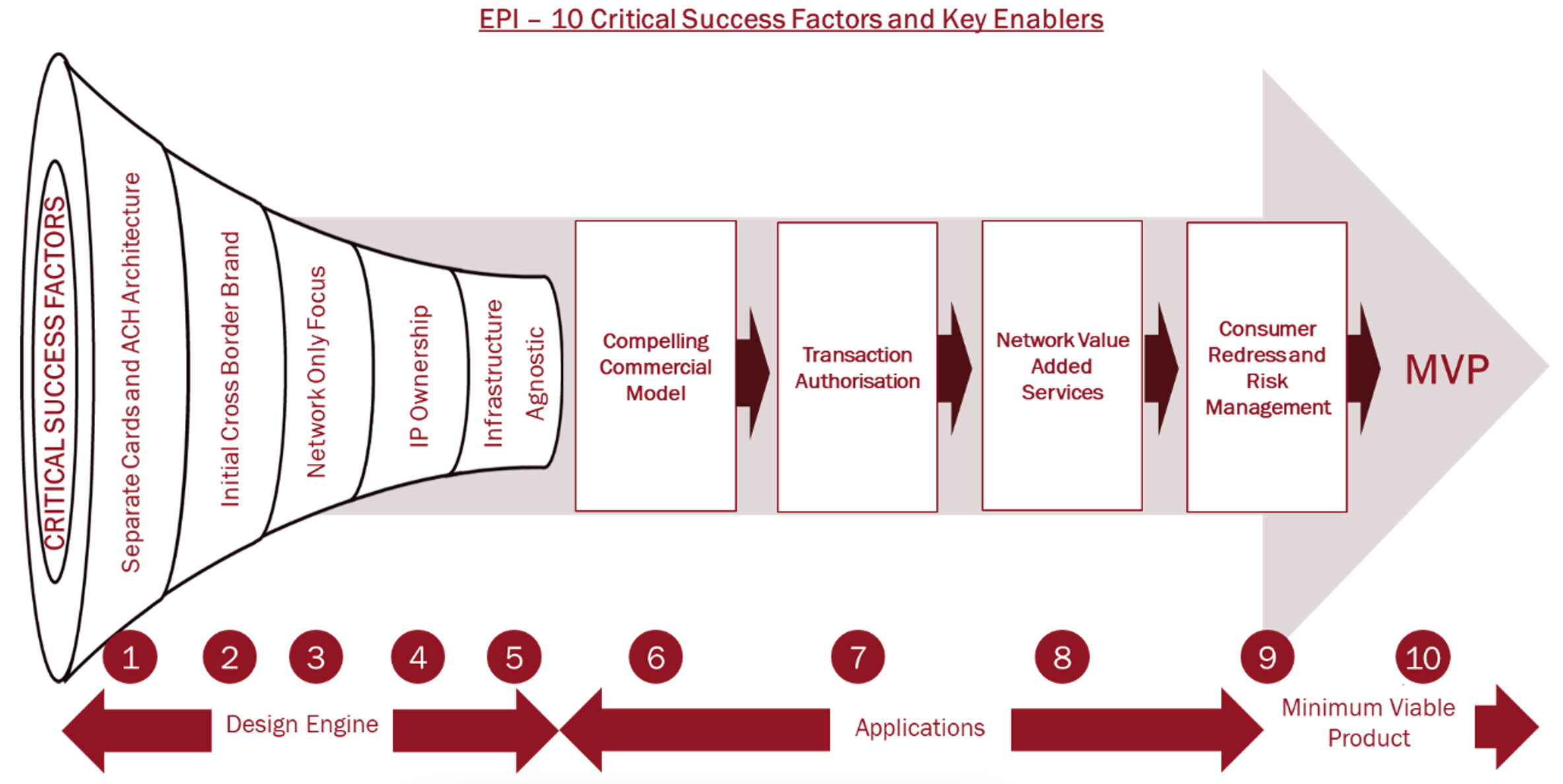

EPI – 10 Critical Success Factors and Key Enablers

Ever since Europe lost EuroPay in the late 1990s, payments stakeholders have been dismayed at the steady decline in their domestic debit card schemes and the gradual displacement of usage (now 70%) in markets where they remain. Several replacement plans have failed, either through lack of support or funding and regulatory concerns. Many have despaired over Europe’s inability to compete with American and Asian schemes and build a sovereign card payments network. Consequently, the European Payment Initiative (EPI) led by 20+ EU banks and processors must be strongly applauded as a bold and visionary concept to create a modern scheme and network for EU citizens, corporates and the financial sector.

Europe has a world class track record of delivering electronic payments process standardisation through the SEPA project. However, SEPA for Cards has struggled for many years to gain development traction. The EPI stakeholders have now recognised the need for a novel structure to deliver a new European scheme by forming a separate EPI company.

However, the scope of the EPI payments vision is very wide. Once requirements are specified the project delivery plan will be potentially very ambitious. Research into similar highly complex interbank initiatives that encountered difficulties in the past, shows uncomfortable parallels. The risks of lack of take up or an extended delivery timeframe and cost overruns are relatively high.

For these reasons, the nine members of the European Payments Consulting Association (EPCA) have developed a list of suggested Critical Success Factors (CSFs) and Key Enablers that can be considered as EPI design the architecture, define applications and agree a Minimum Viable Product (MVP) for the new EU scheme.

1. Separate Cards and ACH. As is well known, the retail cards business ‘technical and operational’ model is highly complex with multifeatured components built around tested security risk management and consumer redress frictionless processing principles developed over 50 years. Building an integrated Electronic Payments (ACH) and sophisticated modern Cards Architecture is a pioneering project yet to be undertaken by interbank scheme developers. The beguiling simplicity of starting within the SCTinst framework to deliver the front and middle components (with P2P as the first implementation) overlooks the potential to become a structure beset with compromises and workarounds. A strong case can be made for a clean sheet design for a pureplay cards architecture using electronic payments only for CSM clearing and settlement. It will be important to learn from the recent modern platforms developed in Russia, Turkey and several EU domestic markets.

2. Cross Border Brand. Since the 1990s, Europe has invested heavily in developing its remaining seven domestic debit card schemes. However, over time it has become increasingly apparent that co-badging with International Card Scheme (ICS) brands for cross border usage has contributed to issuer brand switching. Thus, logic argues that any new pan EU scheme should first focus on resolving the branding issue with a Phase 1 simple architecture. A key CSF would be to initially implement EPI as a cross border co-badge, allowing time for domestic scheme rules to be harmonised and postpone domestic brand absorption into the EPI scheme to a later release. The differences between the schemes in Belgium, Denmark, France, Italy, Portugal and Spain are modest. Germany’s unique Girocard scheme (already undergoing consolidation with other services) will be most impacted by EPI, will need significant change and will benefit from the extended timeframe.

3. Network Only Focus. The ICS have concentrated a very high proportion of their investment in building and expanding their core networks and ensuring easy connectivity in each country. By this means, they have avoided the complexities and costs of developing in-country platforms, domestic market wallets and issuer/acquirer services. It is suggested that EPI should similarly focus initially on designing and building a basic core network (much as the ICS approach) leaving local processing to domestic commercial and interbank processors. This will reduce complexity, limit the risk of cost overruns, ensure continued domestic sovereignty as well as the retention of local payments assets, skills and resources.

4. IP Ownership. Sovereignty is not just about owning a scheme and brand. It is also about ownership of the underlying Intellectual Property (IP) related to the standards, network and service delivery components. All the major payments players and schemes own their IP as a fundamental policy. Ownership enables the construction of competitive Unique Selling Propositions (USPs), provides the agility and flexibility needed to implement rapid change and control release priorities. Although costly, IP ownership is a vital long-term enabler of a successful competitive scheme network development and delivery strategy.

5. Infrastructure Agnostic. As a result of the PSD/IFR and other EU legislation, the new EPI scheme will be obliged to decouple from its delivery service. An important CSF will be to ensure that any processing service avoids dependence and capture through a long-term contract by a single service supplier. Operational network control is a long-established policy of the super payments players, including the ICS and several EU regional and domestic schemes. Outsourcing network processing to a commercial provider has attractions for a low cost faster-to-market solution. However, the platforms and services of many of Europe’s payments processors are primarily designed to support domestic schemes. Inevitably, adaptation to accommodate a modern EPI scheme will involve design compromises. A Key Enabler is for EPI to identify a neutral processor owner and avoid supplier dependence.

6. Compelling Commercial Model. Over and above the strategic and sovereign objectives of the EPI initiative, the new scheme also needs a strong and compelling business case as a CSF to incentivise both issuers to migrate from domestic or ICS brands and acquirers to enable acceptance. Capped debit interchange will be an important ingredient in the EPI commercial model to deliver issuer benefits. However, even if interchange were to be reduced to zero by regulators, ICS scheme fees generate high revenues which enable strong issuer switching and brand retention marketing incentives. Therefore, EPI has an opportunity to undercut ICS scheme fees (which currently average 0.20%) with highly competitive rates at less than 0.05% provided development costs are contained.

7. Authorisation Processes. One of the most important design differences between SCTinst and cards payments is merchant use of a separate acquirer to issuer authorisation step for each card transaction. Single message architectures linked to Instant Payments are simpler, dematerialise batch clearing submission and enable real time settlement. However, card authorisation delivers significant value to consumers and merchants, not just for managing risk/reducing fraud, andsupporting specialist sectors (such as the petroleum), but also by using pre-authorisation to revalidate stored cards on file for merchant initiated recurring payments. In addition, many merchants value the batch clearing submission process and few (if any) would welcome one-to-one transaction settlement. A Key Enabler would be to build a card scheme and network which offers both single and dual messaging.

8. Value Added Services (VAS). The major ICS offer a wide range of ‘in network VAS’ to merchants, acquirers and issuers to enable eCommerce, POS acceptance and risk management. These range from fraud monitoring, account updating/validation, recurring payments, chargeback processing, tokenisation and many more. Both schemes have invested substantially and offer 45/50 network embedded VAS, some of which have become essential services particularly for the issuing business. Despite their high cost, recognising the 6/7 core VAS features and focussing on their development will be an important Key Enabler for the success of the EPI scheme proposition if issuers are to be persuaded to switch brands.

9. Consumer Redress and Risk Management. Electronic ACH payments are a newcomer to POS and eCommerce payments and as a result have not been purpose-built to manage the unique fraud risks, counterparty risk and consumer redress requirements (including transaction repudiation) of day-to-day retail payments. It is proposed that any new European card scheme should have consumer redress processes embedded end to end, including frictionless refunds, chargebacks and product liability as vital application features. Similarly, for merchants and acquirers, the payments guarantee and merchant default monitoring are essential scheme components.

10. Minimum Viable Product (MVP). Finally, it is suggested that a primary success factor for EPI will be to develop a Minimum Viable Product (MVP) for the initial card scheme, design, build and delivery. The Phase 1 deliverables focus should be as card-centric as possible, avoid interference factors from applications not clearly aligned and which have potential to be a diversion from the development of the core card scheme. Ideally, the Phase 1 MVP should only deliver core central card network functionality.

The EPCA believes that whilst these 10 messages may seem like motherhood and apple pie, history tells us that many complex payments development projects rapidly suffer from uncontrollable “application scope explosion”. Designers often fail to appreciate the need for pragmatism and the simple clear vision and design attributes needed to ensure low risk and delivery on time and to budget.

EPI is in a unique position to design and deliver another World Class payments initiative but will only succeed with strong focussed management and an agile methodology which limits the scope of its strategic architecture and operating models for the new scheme and network.

The European Payments Consulting Association (EPCA) is a Pan EU network of independent payments consultants created in 1998 and have an aggregate turnover of €20m, over 500 clients and 80 payments consulting professionals. https://europeanpaymentadvisors.com

Date: 23.12.2020

This year Christmas came white

2020 was the year of challenges and new learnings. We have learned that many things that seemed hard in the past are now part of our daily routines. Things that were challenging – are not that challenging at all. May this knowledge stay with us! Merry Christmas and Happy New year!

Date: 08.07.2020

Staying together even being remote

After some time of self-isolation we went to the seaside to celebrate 8,5 years together. Recent pandemic has given us understanding about joy we share of being together and consulting our customers.

Being part of EPCA family allows us to offer our customers a wider range of financial field topics starting with strategic consulting, payments infrastructure and organization, continuing with development of payment products, financial modelling and business-case calculations, concluding with research and financial analyses.

Date: 11.06.2020

EPCA news

Vedicard is proud to present result tight cooperation among all EPCA members – updated logo, improved web page and linkedIn.

The European Payments Consulting Association (EPCA) is a European network of independent payments consulting companies, who cooperate in offering advisory services to international and Pan European payments industry players and merchants. The EPCA network has the full range of capabilities to meet the needs of international payments companies. Members have over 22 years experience of working together to deliver assignments to Europe’s payments businesses.

In cooperation with EPCA Vedicard is able to provide it’s customers expertise that is obtained by each EPCA member.

Date: 27.11.2019

Vedicard in EPCA (European Payments Consulting Association) Bi-Annual meeting

Vedicard participated in bi-annual European Payments Consulting Association meeting where latest trends in Payments consulting and future development plans and ideas were shared. Work in progress to enhance payments consulting in Europe and Vedicard is happy to be part of that.

Date: 05.11.2019

Vedicard joins Latvian Chamber of Commerce and Industry

Latvian Chamber of Commerce and Industry is the biggest association of entrepreneurs in Latvia uniting more than 2500 members – micro, small, medium and large enterprises of all regions and industries, associations, city business clubs and other unions of entrepreneurs. Association represents interests of entrepreneurs, as well as provides services, so that Latvia has excellent enterprises in an excellent business environment. Main sectors of its activities are business environment, competitiveness of enterprises, export.

Date:

02.10.2019

MCDS Market shaker Award

Vedicard has been presented MCDS Market Shaker Award for Priceless contribution in the development of a cashless payments society! Feeling honoured and very happy for our work recognition from MasterCard!